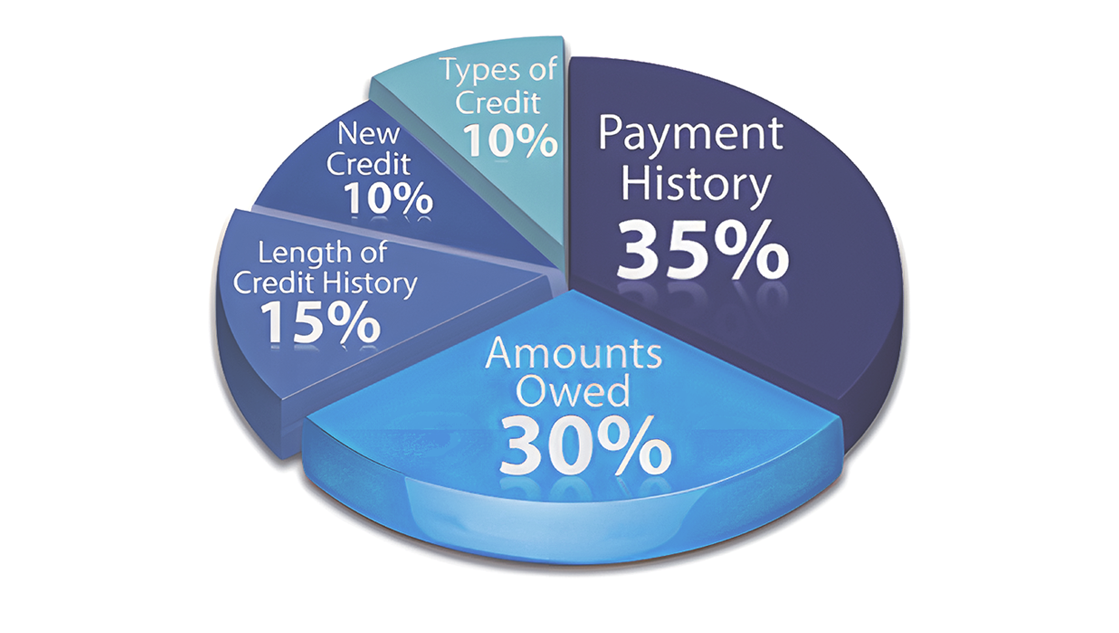

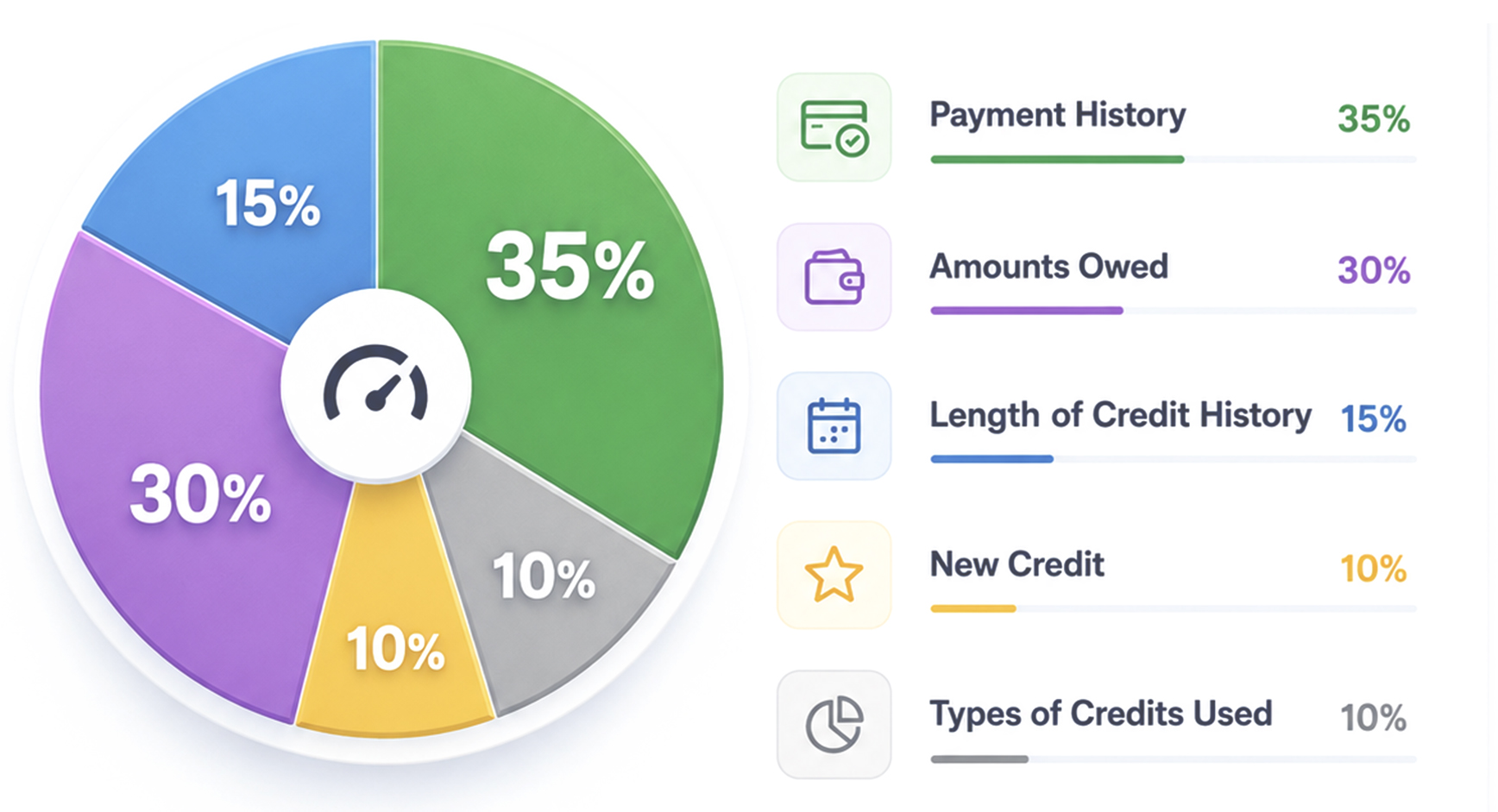

1) Highest impact • ~35% of FICO®

Payment history

Your record of paying credit accounts on time—including 30/60/90-day lates, collections, charge-offs, and any serious derogatory events.

Shopping for a home, car, or business funding? Your credit score matters—but it isn’t the only input. Lenders also look at your mix of accounts, new activity, and how you’ve managed credit over time.

Quick view of weights (FICO®): Payment history ~35% · Utilization ~30% · Length of history ~15% · New credit ~10% · Credit mix ~10%.

1) Highest impact • ~35% of FICO®

Your record of paying credit accounts on time—including 30/60/90-day lates, collections, charge-offs, and any serious derogatory events.

2) High impact • ~30% of FICO®

How much of your available credit you use—overall and on each card. Also considers how many accounts report balances and loan balances vs. original amounts.

3) Moderate impact • ~15% of FICO®

Age of your oldest and newest accounts, the average age of accounts, and time since last activity. This factor strengthens naturally over time.

4) Lower impact • ~10% of FICO®

Recent activity: hard inquiries and newly opened accounts. Many new accounts in a short time indicate higher risk and can also reduce average age.

5) Lower impact • ~10% of FICO®

The variety of accounts you manage—revolving (cards/retail), installment (auto/student/personal), mortgage, etc.

Pair Meta Fiscal’s hands-on guidance with continuous monitoring to track progress and respond quickly.

Join our newsletter for clear insights designed to help you make informed credit and financial decisions.

Why join the journal

Brief, practical guidance created to help you understand your financial profile and make smarter decisions.

Loan Education

Loan Education

Understand what a denial may mean and how to move forward without guessing.

Explore the journal Credit Education

Credit Education

Learn the core factors that influence your credit score and which financial habits matter most.

Explore the journal Credit Education

Credit Education

See what different score ranges may mean and understand where your profile currently stands.

Explore the journal Client Education

Client Education

Learn which common decisions may slow your progress and how to protect the work already underway.

Explore the journal Funding Readiness

Funding Readiness

Understand the business and financial factors lenders may review before making a funding decision.

Explore the journal Affiliate Program

Affiliate Program

Learn how the Meta Fiscal affiliate program can turn trusted introductions into an additional income stream.

Explore the journal