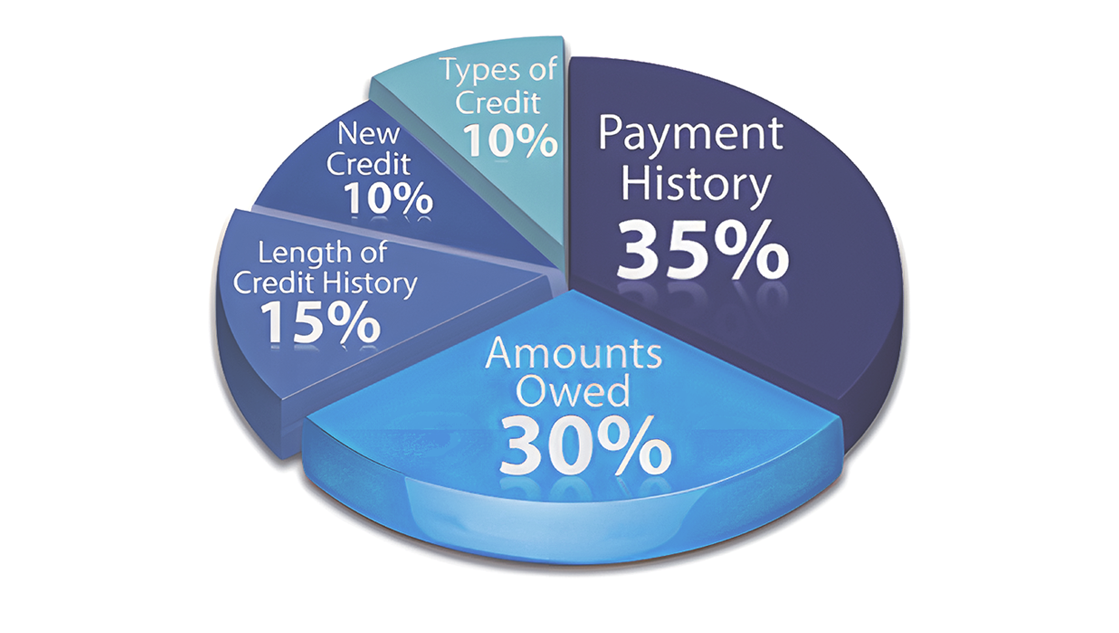

1) Payment History

Highest impact • ~35% of FICO®

What it is

Your record of paying accounts on time (late payments, collections, charge-offs, bankruptcies).

Credit impact

Largest weight (~35%). Recent/frequent/severe delinquencies hurt most; clean history powers the highest scores.

How it’s calculated

Severity (30/60/90+), recency, frequency, and derogatory public records/collections.

Healthy benchmark

100% on-time payments; no past-due balances.

How to improve

Autopay at least the minimum, reminders, bring delinquencies current, prevent bills from going to collections.

Common pitfalls

One-day-late payments, forgetting small/medical bills, assuming deferments always report as “on-time.”

2) Amounts Owed (Utilization)

High impact • ~30% of FICO®

What it is

How much of your available credit you use—especially on revolving credit cards.

Credit impact

~30% weight. Higher utilization = higher risk. Both overall and per-card utilization matter.

How it’s calculated

Overall revolving utilization, per-card utilization, number of accounts with balances, and installment loan balances vs. original amounts.

Healthy benchmark

<30% overall and per card; single digits (<10%) ideal for top scores.

How to improve

Pay before statement close, make mid-cycle payments, responsibly raise limits, avoid maxing out; don’t close good cards you use.

Common pitfalls

Letting one card report 80–100%, closing a card and shrinking total limit, thinking you must “carry” a balance (you don’t).

3) Length of Credit History

Moderate impact • ~15% of FICO®

What it is

How long you’ve used credit: oldest, newest, and average age of accounts, plus time since last activity.

Credit impact

~15% weight. Longer, positive histories are favored; grows with time.

How it’s calculated

Combines age of oldest/newest accounts with average age and recent activity.

Healthy benchmark

Preserve long-standing accounts in good standing; keep them lightly active.

How to improve

Avoid closing your oldest healthy cards; consider product-change instead of closing to keep history.

Common pitfalls

Opening several new cards at once (drops average age), closing your oldest card, long inactivity.

4) New Credit

Lower impact • ~10% of FICO®

What it is

Recent hard inquiries and newly opened accounts.

Credit impact

~10% weight. Hard pulls are small/temporary; new accounts can also reduce average age.

How it’s calculated

Counts hard inquiries (last ~12 months) and new accounts. Rate-shopping (mortgage/auto/student) within a short window is treated as one inquiry by many FICO versions.

Healthy benchmark

Apply only as needed; cluster loan quotes in a short window; use soft-pull prequal where possible.

How to improve

Space out applications; avoid opening several cards at once; let inquiries age off.

Common pitfalls

Multiple card apps in a month; assuming all pulls are soft; mixing many account types at once.

5) Credit Mix

Lower impact • ~10% of FICO®

What it is

The variety of accounts you manage—revolving (cards/retail), installment (auto/student/personal), mortgage, etc.

Credit impact

~10% weight. Demonstrating you can manage different types helps at the margin; not required to have everything.

How it’s calculated

Types present and your track record with them. Strong payment history outweighs having many types.

Healthy benchmark

At least one active revolving account in good standing; mix grows naturally with needs (auto, mortgage).

How to improve

Don’t open debt just for “mix.” Keep a low-utilization card active; let installment loans age and pay on time.

Common pitfalls

Closing your last credit card; opening finance-company accounts you don’t need.

Next step

Track & improve

Ready to apply this? Monitor your profile and act fast when things change.