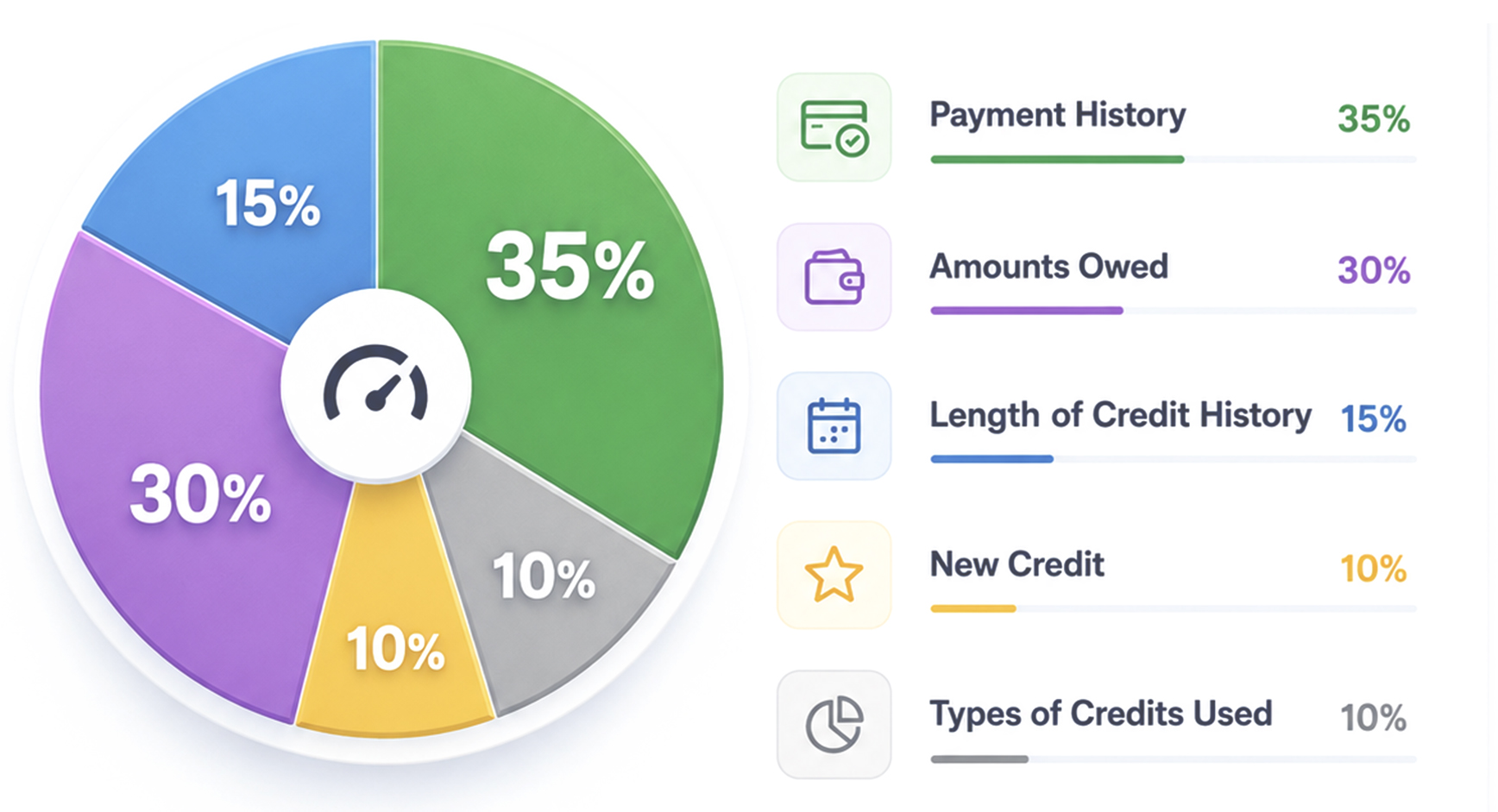

35%

Payment History

Largest Factor

Payment History

Your payment history is usually one of the most important parts of your credit profile. Late payments, charge-offs, collections, and missed accounts may negatively affect your score.

What May Help

- Pay all current accounts on time

- Address inaccurate negative reporting

- Avoid falling behind on active accounts

- Create consistent payment habits